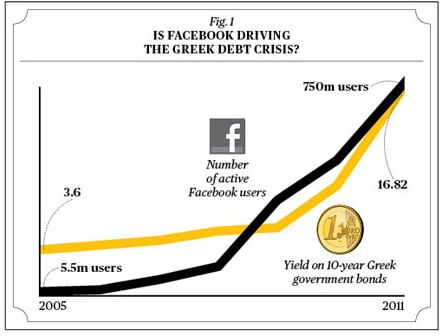

It is a commonplace of scientific discussion that correlation does not imply causation. Business Week recently ran an spoof article pointing out some amusing examples of the dangers of inferring causation from correlation. For example, the article points out that Facebook’s growth has been strongly correlated with the yield on Greek government bonds: (credit)

Despite this strong correlation, it would not be wise to conclude that the success of Facebook has somehow caused the current (2009-2012) Greek debt crisis, nor that the Greek debt crisis has caused the adoption of Facebook!

Of course, while it’s all very well to piously state that correlation doesn’t imply causation, it does leave us with a conundrum: under what conditions, exactly, can we use experimental data to deduce a causal relationship between two or more variables?

The standard scientific answer to this question is that (with some caveats) we can infer causality from a well designed randomized controlled experiment. Unfortunately, while this answer is satisfying in principle and sometimes useful in practice, it’s often impractical or impossible to do a randomized controlled experiment. And so we’re left with the question of whether there are other procedures we can use to infer causality from experimental data. And, given that we can find more general procedures for inferring causal relationships, what does causality mean, anyway, for how we reason about a system?

It might seem that the answers to such fundamental questions would have been settled long ago. In fact, they turn out to be surprisingly subtle questions. Over the past few decades, a group of scientists have developed a theory of causal inference intended to address these and other related questions. This theory can be thought of as an algebra or language for reasoning about cause and effect. Many elements of the theory have been laid out in a famous book by one of the main contributors to the theory, Judea Pearl. Although the theory of causal inference is not yet fully formed, and is still undergoing development, what has already been accomplished is interesting and worth understanding.

In this post I will describe one small but important part of the theory of causal inference, a causal calculus developed by Pearl. This causal calculus is a set of three simple but powerful algebraic rules which can be used to make inferences about causal relationships. In particular, I’ll explain how the causal calculus can sometimes (but not always!) be used to infer causation from a set of data, even when a randomized controlled experiment is not possible. Also in the post, I’ll describe some of the limits of the causal calculus, and some of my own speculations and questions.

The post is a little technically detailed at points. However, the first three sections of the post are non-technical, and I hope will be of broad interest. Throughout the post I’ve included occasional “Problems for the author”, where I describe problems I’d like to solve, or things I’d like to understand better. Feel free to ignore these if you find them distracting, but I hope they’ll give you some sense of what I find interesting about the subject. Incidentally, I’m sure many of these problems have already been solved by others; I’m not claiming that these are all open research problems, although perhaps some are. They’re simply things I’d like to understand better. Also in the post I’ve included some exercises for the reader, and some slightly harder problems for the reader. You may find it informative to work through these exercises and problems.

Before diving in, one final caveat: I am not an expert on causal inference, nor on statistics. The reason I wrote this post was to help me internalize the ideas of the causal calculus. Occasionally, one finds a presentation of a technical subject which is beautifully clear and illuminating, a presentation where the author has seen right through the subject, and is able to convey that crystalized understanding to others. That’s a great aspirational goal, but I don’t yet have that understanding of causal inference, and these notes don’t meet that standard. Nonetheless, I hope others will find my notes useful, and that experts will speak up to correct any errors or misapprehensions on my part.

Simpson’s paradox

Let me start by explaining two example problems to illustrate some of the difficulties we run into when making inferences about causality. The first is known as Simpson’s paradox. To explain Simpson’s paradox I’ll use a concrete example based on the passage of the Civil Rights Act in the United States in 1964.

In the US House of Representatives, 61 percent of Democrats voted for the Civil Rights Act, while a much higher percentage, 80 percent, of Republicans voted for the Act. You might think that we could conclude from this that being Republican, rather than Democrat, was an important factor in causing someone to vote for the Civil Rights Act. However, the picture changes if we include an additional factor in the analysis, namely, whether a legislator came from a Northern or Southern state. If we include that extra factor, the situation completely reverses, in both the North and the South. Here’s how it breaks down:

North: Democrat (94 percent), Republican (85 percent)

South: Democrat (7 percent), Republican (0 percent)

Yes, you read that right: in both the North and the South, a larger fraction of Democrats than Republicans voted for the Act, despite the fact that overall a larger fraction of Republicans than Democrats voted for the Act.

You might wonder how this can possibly be true. I’ll quickly state the raw voting numbers, so you can check that the arithmetic works out, and then I’ll explain why it’s true. You can skip the numbers if you trust my arithmetic.

North: Democrat (145/154, 94 percent), Republican (138/162, 85 percent)

South: Democrat (7/94, 7 percent), Republican (0/10, 0 percent)

Overall: Democrat (152/248, 61 percent), Republican (138/172, 80 percent)

One way of understanding what’s going on is to note that a far greater proportion of Democrat (as opposed to Republican) legislators were from the South. In fact, at the time the House had 94 Democrats, and only 10 Republicans. Because of this enormous difference, the very low fraction (7 percent) of southern Democrats voting for the Act dragged down the Democrats’ overall percentage much more than did the even lower fraction (0 percent) of southern Republicans who voted for the Act.

(The numbers above are for the House of Congress. The numbers were different in the Senate, but the same overall phenomenon occurred. I’ve taken the numbers from Wikipedia’s article about Simpson’s paradox, and there are more details there.)

If we take a naive causal point of view, this result looks like a paradox. As I said above, the overall voting pattern seems to suggest that being Republican, rather than Democrat, was an important causal factor in voting for the Civil Rights Act. Yet if we look at the individual statistics in both the North and the South, then we’d come to the exact opposite conclusion. To state the same result more abstractly, Simpson’s paradox is the fact that the correlation between two variables can actually be reversed when additional factors are considered. So two variables which appear correlated can become anticorrelated when another factor is taken into account.

You might wonder if results like those we saw in voting on the Civil Rights Act are simply an unusual fluke. But, in fact, this is not that uncommon. Wikipedia’s page on Simpson’s paradox lists many important and similar real-world examples ranging from understanding whether there is gender-bias in university admissions to which treatment works best for kidney stones. In each case, understanding the causal relationships turns out to be much more complex than one might at first think.

I’ll now go through a second example of Simpson’s paradox, the kidney stone treatment example just mentioned, because it helps drive home just how bad our intuitions about statistics and causality are.

Imagine you suffer from kidney stones, and your Doctor offers you two choices: treatment A or treatment B. Your Doctor tells you that the two treatments have been tested in a trial, and treatment A was effective for a higher percentage of patients than treatment B. If you’re like most people, at this point you’d say “Well, okay, I’ll go with treatment A”.

Here’s the gotcha. Keep in mind that this really happened. Suppose you divide patients in the trial up into those with large kidney stones, and those with small kidney stones. Then even though treatment A was effective for a higher overall percentage of patients than treatment B, treatment B was effective for a higher percentage of patients in both groups, i.e., for both large and small kidney stones. So your Doctor could just as honestly have said “Well, you have large [or small] kidney stones, and treatment B worked for a higher percentage of patients with large [or small] kidney stones than treatment A”. If your Doctor had made either one of these statements, then if you’re like most people you’d have decided to go with treatment B, i.e., the exact opposite treatment.

The kidney stone example relies, of course, on the same kind of arithmetic as in the Civil Rights Act voting, and it’s worth stopping to figure out for yourself how the claims I made above could possibly be true. If you’re having trouble, you can click through to the Wikipedia page, which has all the details of the numbers.

Now, I’ll confess that before learning about Simpson’s paradox, I would have unhesitatingly done just as I suggested a naive person would. Indeed, even though I’ve now spent quite a bit of time pondering Simpson’s paradox, I’m not entirely sure I wouldn’t still sometimes make the same kind of mistake. I find it more than a little mind-bending that my heuristics about how to behave on the basis of statistical evidence are obviously not just a little wrong, but utterly, horribly wrong.

Perhaps I’m alone in having terrible intuition about how to interpret statistics. But frankly I wouldn’t be surprised if most people share my confusion. I often wonder how many people with real decision-making power – politicians, judges, and so on – are making decisions based on statistical studies, and yet they don’t understand even basic things like Simpson’s paradox. Or, to put it another way, they have not the first clue about statistics. Partial evidence may be worse than no evidence if it leads to an illusion of knowledge, and so to overconfidence and certainty where none is justified. It’s better to know that you don’t know.

Correlation, causation, smoking, and lung cancer

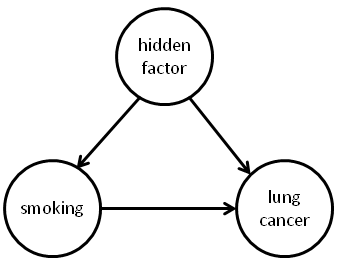

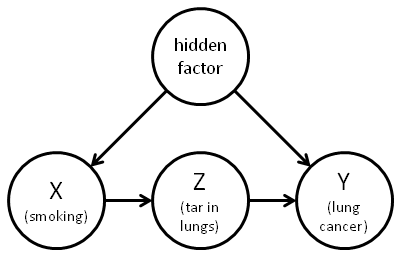

As a second example of the difficulties in establishing causality, consider the relationship between cigarette smoking and lung cancer. In 1964 the United States’ Surgeon General issued a report claiming that cigarette smoking causes lung cancer. Unfortunately, according to Pearl the evidence in the report was based primarily on correlations between cigarette smoking and lung cancer. As a result the report came under attack not just by tobacco companies, but also by some of the world’s most prominent statisticians, including the great Ronald Fisher. They claimed that there could be a hidden factor – maybe some kind of genetic factor – which caused both lung cancer and people to want to smoke (i.e., nicotine craving). If that was true, then while smoking and lung cancer would be correlated, the decision to smoke or not smoke would have no impact on whether you got lung cancer.

Now, you might scoff at this notion. But derision isn’t a principled argument. And, as the example of Simpson’s paradox showed, determining causality on the basis of correlations is tricky, at best, and can potentially lead to contradictory conclusions. It’d be much better to have a principled way of using data to conclude that the relationship between smoking and lung cancer is not just a correlation, but rather that there truly is a causal relationship.

One way of demonstrating this kind of causal connection is to do a randomized, controlled experiment. We suppose there is some experimenter who has the power to intervene with a person, literally forcing them to either smoke (or not) according to the whim of the experimenter. The experimenter takes a large group of people, and randomly divides them into two halves. One half are forced to smoke, while the other half are forced not to smoke. By doing this the experimenter can break the relationship between smoking and any hidden factor causing both smoking and lung cancer. By comparing the cancer rates in the group who were forced to smoke to those who were forced not to smoke, it would then be possible determine whether or not there is truly a causal connection between smoking and lung cancer.

This kind of randomized, controlled experiment is highly desirable when it can be done, but experimenters often don’t have this power. In the case of smoking, this kind of experiment would probably be illegal today, and, I suspect, even decades into the past. And even when it’s legal, in many cases it would be impractical, as in the case of the Civil Rights Act, and for many other important political, legal, medical, and econonomic questions.

Causal models

To help address problems like the two example problems just discussed, Pearl introduced a causal calculus. In the remainder of this post, I will explain the rules of the causal calculus, and use them to analyse the smoking-cancer connection. We’ll see that even without doing a randomized controlled experiment it’s possible (with the aid of some reasonable assumptions) to infer what the outcome of a randomized controlled experiment would have been, using only relatively easily accessible experimental data, data that doesn’t require experimental intervention to force people to smoke or not, but which can be obtained from purely observational studies.

To state the rules of the causal calculus, we’ll need several background ideas. I’ll explain those ideas over the next three sections of this post. The ideas are causal models (covered in this section), causal conditional probabilities, and d-separation, respectively. It’s a lot to swallow, but the ideas are powerful, and worth taking the time to understand. With these notions under our belts, we’ll able to understand the rules of the causal calculus

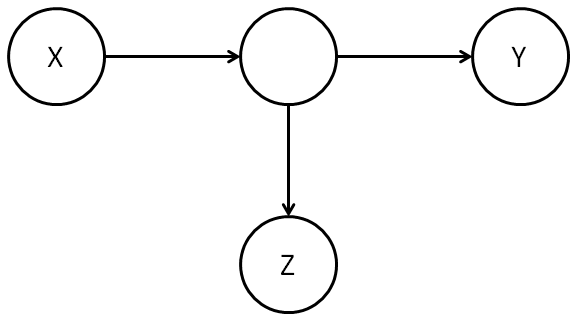

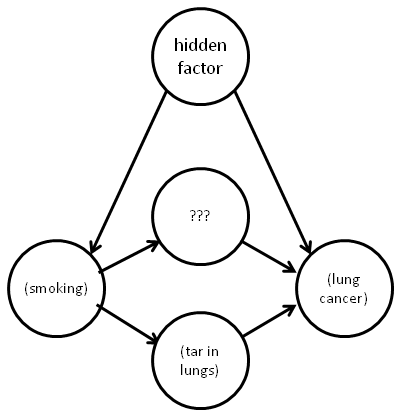

To understand causal models, consider the following graph of possible causal relationships between smoking, lung cancer, and some unknown hidden factor (say, a hidden genetic factor):

This is a quite general model of causal relationships, in the sense that it includes both the suggestion of the US Surgeon General (smoking causes cancer) and also the suggestion of the tobacco companies (a hidden factor causes both smoking and cancer). Indeed, it also allows a third possibility: that perhaps both smoking and some hidden factor contribute to lung cancer. This combined relationship could potentially be quite complex: it could be, for example, that smoking alone actually reduces the chance of lung cancer, but the hidden factor increases the chance of lung cancer so much that someone who smokes would, on average, see an increased probability of lung cancer. This sounds unlikely, but later we’ll see some toy model data which has exactly this property.

Of course, the model depicted in the graph above is not the most general possible model of causal relationships in this system; it’s easy to imagine much more complex causal models. But at the very least this is an interesting causal model, since it encompasses both the US Surgeon General and the tobacco company suggestions. I’ll return later to the possibility of more general causal models, but for now we’ll simply keep this model in mind as a concrete example of a causal model.

Mathematically speaking, what do the arrows of causality in the diagram above mean? We’ll develop an answer to that question over the next few paragraphs. It helps to start by moving away from the specific smoking-cancer model to allow a causal model to be based on a more general graph indicating possible causal relationships between a number of variables:

Each vertex in this causal model has an associated random variable,

A notational convention that we’ll use often is to interchangeably use

For the notion of causality to make sense we need to constrain the class of graphs that can be used in a causal model. Obviously, it’d make no sense to have loops in the graph:

We can’t have

By the way, I must admit that I’m not a fan of the term directed acyclic graph. It sounds like a very complicated notion, at least to my ear, when what it means is very simple: a graph with no loops. I’d really prefer to call it a “loop-free graph”, or something like that. Unfortunately, the “directed acyclic graph” nomenclature is pretty standard, so we’ll go with it.

Our picture so far is that a causal model consists of a directed acyclic graph, whose vertices are labelled by random variables

Intuitively, what causality means is that for any particular }")

} = (X_2,X_3)")

Now, of course, vertices further back in the graph – say, the parents of the parents – could, of course, influence the value of

Note, by the way, that I’ve overloaded the }")

Motivated by the above discussion, one way we could define causal influence would be to require that

}),")

where ")

},Y_{j,1},Y_{j,2},\ldots),")

where

Summing up, a causal model consists of a directed acyclic graph,

},Y_{j,\cdot})")

In practice, we will not work directly with the functions

= \prod_j p(x_j | \mbox{pa}(x_j)).")

I won’t prove this equation, but the expression should be plausible, and is pretty easy to prove; I’ve asked you to prove it as an optional exercise below.

Exercises

- Prove the above equation for the joint probability distribution.

Problems

- (Simpson’s paradox in causal models) Consider the causal model of smoking introduced above. Suppose that the hidden factor is a gene which is either switched on or off. If on, it tends to make people both smoke and get lung cancer. Find explicit values for conditional probabilities in the causal model such that

, and yet if the additional genetic factor is taken into account this relationship is reversed. That is, we have both

and

.

Problems for the author

- An alternate, equivalent approach to defining causal models is as follows: (1) all root vertices (i.e., vertices with no parents) in the graph are labelled by independent random variables. (2) augment the graph by introducing new vertices corresponding to the

. These new vertices have single outgoing edges, pointing to

I’ve been using terms like “causal influence” somewhat indiscriminately in the discussion above, and so I’d like to pause to discuss a bit more carefully about what is meant here, and what nomenclature we should use going forward. All the arrows in a causal model indicate are the possibility of a direct causal influence. This results in two caveats on how we think about causality in these models. First, it may be that a child random variable is actually completely independent of the value of one (or more) of its parent random variables. This is, admittedly, a rather special case, but is perfectly consistent with the definition. For example, in a causal model like

it is possible that the outcome of cancer might be independent of the hidden causal factor or, for that matter, that it might be independent of whether someone smokes or not. (Indeed, logically, at least, it may be independent of both, although of course that’s not what we’ll find in the real world.) The second caveat in how we think about the arrows and causality is that the arrows only capture the direct causal influences in the model. It is possible that in a causal model like

Causal conditional probabilities

In this section I’ll explain what I think is the most imaginative leap underlying the causal calculus. It’s the introduction of the concept of causal conditional probabilities.

The notion of ordinary conditional probabilities is no doubt familiar to you. It’s pretty straightforward to do experiments to estimate conditional probabilities such as ")

As we discussed earlier, what you’d really like to do in this circumstance is a randomized controlled experiment in which it’s possible for the experimenter to force someone to smoke (or not smoke), breaking the causal connection between the hidden factor and smoking. In such an experiment you really could see if there was a causal influence by looking at what fraction of people who smoked got cancer. In particular, if that fraction was higher than in the overall population then you’d be justified in concluding that smoking helped cause cancer. In practice, it’s probably not practical to do this kind of randomized controlled experiment. But Pearl had what turns out to be a very clever idea: to imagine a hypothetical world in which it really is possible to force someone to (for example) smoke, or not smoke. In particular, he introduced a conditional causal probability })")

Now, at first sight this appears a rather useless thing to do. But what makes it a clever imaginative leap is that although it may be impossible or impractical to do a controlled experiment to determine )")

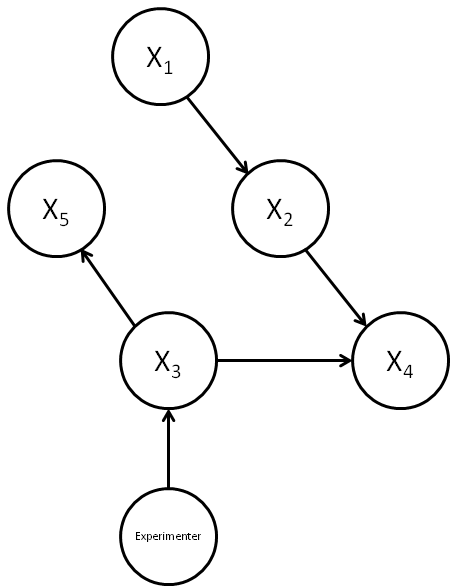

We’ll discuss the rules of the causal calculus later in this post. For now, though, let’s develop the notion of causal conditional probabilities. Suppose we have a causal model of some phenomenon:

Now suppose we introduce an external experimenter who is able to intervene to deliberately set the value of a particular variable

In this new causal model, we’ve represented the experimenter by a new vertex, which has as a child the vertex

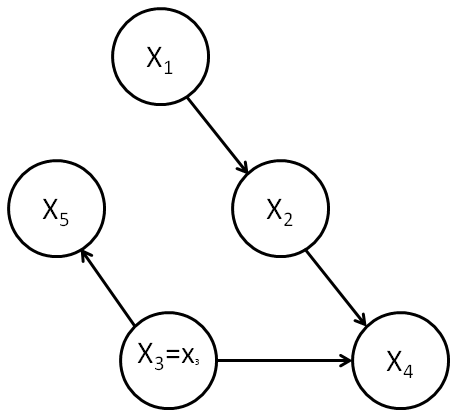

This model has no vertex explicitly representing the experimenter, but rather the relation ")

")

Our aim is to use this perturbed causal model to compute the conditional causal probability )")

")

= \prod_k p(x_k| \mbox{pa}(x_k)),")

where the product on the right is over all vertices in the causal model. This expression remains true for the perturbed causal model, but a single term on the right-hand side changes: the conditional probability for the )")

) = \frac{p(x_1,\ldots,x_n)}{p(x_j|\mbox{pa}(x_j))}.")

This equation is a fundamental expression, capturing what it means for an experimenter to intervene to set the value of some particular variable in a causal model. It can easily be generalized to a situation where we partition the variables into two sets,

![[1] \,\,\,\, p(Y=y| \mbox{do}(X=x)) = \frac{p(X=x,Y=y)}{\Pi_j p(X_j = x_j| \mbox{pa}(X_j))}.](https://s0.wp.com/latex.php?latex=+%5B1%5D+%5C%2C%5C%2C%5C%2C%5C%2C+p%28Y%3Dy%7C+%5Cmbox%7Bdo%7D%28X%3Dx%29%29+%3D+%5Cfrac%7Bp%28X%3Dx%2CY%3Dy%29%7D%7B%5CPi_j+p%28X_j+%3D+x_j%7C+++%5Cmbox%7Bpa%7D%28X_j%29%29%7D.++&bg=ffffff&fg=000000&s=0 "[1] \,\,\,\, p(Y=y| \mbox{do}(X=x)) = \frac{p(X=x,Y=y)}{\Pi_j p(X_j = x_j| \mbox{pa}(X_j))}.")

Note that on the right-hand side the values for ")

What we’d like is to compute

All is not lost, however. Just because we can’t compute the expression on the right of [1] directly doesn’t mean we can’t compute causal conditional probabilities in other ways, and we’ll see below how the causal calculus can help solve this kind of problem. It’s not a complete solution – we shall see that it doesn’t always make it possible to compute causal conditional probabilities. But it does help. In particular, we’ll see that although it’s not possible to compute

With causal conditional probabilities defined, we’re now in position to define more precisely what we mean by causal influence. Suppose we have a causal model, and

) \neq p(y|\mbox{do}(x_2))")

Exercises

- (The causal capacity) This exercise is for people with some background in information theory. Suppose we define the causal capacity between

, where

is the mutual information, the maximization is over possible distributions

for

(we use the hat to indicate that the value of

is the corresponding random variable at

. Shannon’s noisy channel coding theorem tells us that an external experimenter who can intervene to set the value of

We’ve just defined a notion of causal influence between two random variables in a causal model. What about when we say something like “Event A” causes “Event B”? What does this mean? Returning to the smoking-cancer example, it seems that we would say that smoking causes cancer provided ) > p(\mbox{cancer})")

Problems for the author

- Suppose

for some pair of values

- (Sum-over-paths for causal conditional probabilities?) I believe a kind of sum-over-paths formulation of causal conditional probabilities is possible, but haven’t worked out details. The idea is as follows (the details may be quite wrong, but I believe something along these lines should work). Supose

, i.e., intervention does nothing. Second, if

may be obtained by summing over all directed paths from

, and computing for each path a contribution to the sum which is a product of conditional probabilities along the path. (Note that we may need to consider the same path multiple times in the sum, since the random variables along the path may take different values).

- We used causal models in our definition of causal conditional probabilities. But our informal definiton – imagine a hypothetical world in which it’s possible to force a variable to take a particular value – didn’t obviously require the use of a causal model. Indeed, in a real-world randomized controlled experiment it may be that there is no underlying causal model. This leads me to wonder if there is some other way of formalizing the informal definition we’ve given?

- Another way of framing the last problem is that I’m concerned about the empirical basis for causal models. How should we go about constructing such models? Are they fundamental, representing true facts about the world, or are they modelling conveniences? (This is by no means a dichotomy.) It would be useful to work through many more examples, considering carefully the origin of the functions

d-separation

In this section we’ll develop a criterion that Pearl calls directional separation (d-separation, for short). What d-separation does is let us inspect the graph of a causal model and conclude that a random variable

To understand d-separation we’ll start with a simple case, and then work through increasingly complex cases, building up our intuition. I’ll conclude by giving a precise definition of d-separation, and by explaining how d-separation relates to the concept of conditional independence of random variables.

Here’s the first simple causal model:

Clearly, knowing

By contrast, in the following causal model

A useful piece of terminology is to say that a vertex like the middle vertex in this model is a collider for the path from

What about the causal model:

In this case, it is possible that knowing

Exercises

- Construct an explicit causal model demonstrating the assertion of the last paragraph. For example, you may construct a causal model in which

- Suppose we have a path from

be the number of colliders along the path, and let

be the number of forks along the path. Show that

can only take the values

or

, i.e., the number of forks and colliders is either the same or differs by at most one.

We’ll say that a path (of any length) from

It’s worth noting that the concepts of d-separation and d-connectedness depend only on the graph topology and on which vertices

With that said, it probably won’t surprise you to learn that the concept of d-separation is closely related to whether or not the random variables

Exercises

- Suppose that

.

- Suppose we have two vertices which are d-connected in a graph

- The last two exercises almost but don’t quite claim that random variables

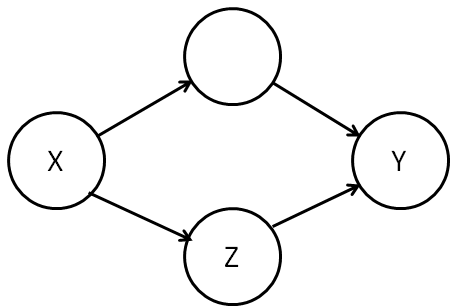

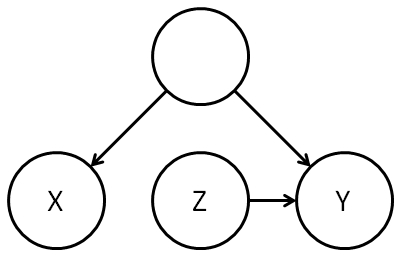

So far, this is pretty simple stuff. It gets more complicated, however, when we extend the notion of d-separation to cases where we are conditioning on already knowing the value of one or more random variables in the causal model. Consider, for example, the graph:

(Figure A.)

Now, if we know

It is helpful to give a name to vertices like the middle vertex in Figure A, i.e., to vertices with one ingoing and one outgoing edge. We’ll call such vertices a traverse along the path from

By contrast, consider this model:

In this case, knowing

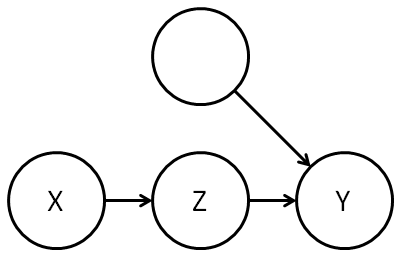

Another case similar to Figure A is the model with a fork:

Again, if we know

The lesson of this model is that if

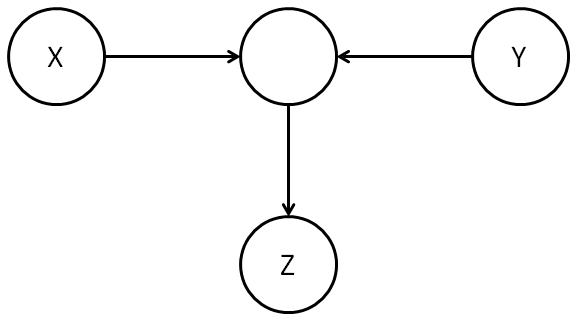

A subtlety arises when we consider a collider:

(Figure B.)

In the unconditioned case this would have been considered a blocked path. And, naively, it seems as though this should still be the case: at first sight (at least according to my intuition) it doesn’t seem very likely that

In fact, we’re wise to be cautious because

Another way of seeing Berkson’s paradox is to construct an explicit causal model for the graph in Figure B. Consider, for example, a causal model in which

As a result of this discussion, in the causal graph of Figure B we’ll say that

The immediate lesson from the graph of Figure B is that

(Figure C.)

To see this, suppose we choose

The general intuition about graphs like that in Figure C is that knowing

Given the discussion of Figure C that we’ve just had, you might wonder why forks or traverses which are ancestors of

The reason, of course, is that it’s easy to construct examples where

These examples motivate the following definition:

Definition: Let

Saying “_G")

_G")

As an aside, Pearl uses a similar but slightly different notation for d-separation, namely _G")

While I’m making asides, let me make a second: when I was first learning this material, I found the “d” for “directional” in d-separation and d-connected rather confusing. It suggested to me that the key thing was having a directed path from one vertex to the other, and that the complexities of colliders, forks, and so on were a sideshow. Of course, they’re not, they’re central to the whole discussion. For this reason, when I was writing these notes I considered changing the terminology to i-separated and i-connected, for informationally-separated and informationally-connected. Ultimately I decided not to do this, but I thought mentioning the issue might be helpful, in part to reassure readers (like me) who thought the “d” seemed a little mysterious.

Okay, that’s enough asides, let’s get back to the main track of discussion.

We saw earlier that (unconditional) d-separation is closely connected to the independence of random variables. It probably won’t surprise you to learn that conditional d-separation is closely connected to conditional independence of random variables. Recall that two sets of random variables  = p(x|z)p(y|z)")

Theorem (graphical criterion for conditional independence): Let

(Update: Thanks to Rob Spekkens for pointing out an error in my original statement of this theorem.)

I won’t prove the theorem here. However, it’s not especially difficult if you’ve followed the discussion above, and is a good problem to work through:

Problems

- Prove the above theorem.

Problems for the author

- The concept of d-separation plays a central role in the causal calculus. My sense is that it should be possible to find a cleaner and more intuitive definition that substantially simplifies many proofs. It’d be good to spend some time trying to find such a definition.

The causal calculus

We’ve now got all the concepts we need to state the rules of the causal calculus. There are three rules. The rules look complicated at first, although they’re easy to use once you get familiar with them. For this reason I’ll start by explaining the intuition behind the first rule, and how you should think about that rule. Having understood how to think about the first rule it’s easy to get the hang of all three rules, and so after that I’ll just outright state all three rules.

In what follows, we have a causal model on a graph

Rule 1: When can we ignore observations: I’ll begin by stating the first rule in all its glory, but don’t worry if you don’t immediately grok the whole rule. Instead, just take a look, and try to start getting your head around it. What we’ll do then is look at some simple special cases, which are easily understood, and gradually build up to an understanding of what the full rule is saying.

Okay, so here’s the first rule of the causal calculus. What it tells us is that when _{G_{\overline X}}")

,z) = p(y|w,\mbox{do}(x))")

To understand why this rule is true, and what it means, let’s start with a much simpler case. Let’s look at what happens to the rule when there are no _G")

= p(y)")

In other words, the first rule is simply a generalization of what it means for

We begin with generalization (1), i.e., there is no  = p(y|w)")

Now let’s look at the other generalization, (2), in which we’ve added an extra variable ,z) = p(y|\mbox{do}(x))")

The full rule, of course, merely combines both these generalizations in the obvious way. It is really just an explicit statement of the content of the graphical criterion for conditional independence, in a context where

The rules of the causal calculus: All three rules of the causal calculus follow a similar template to the first rule: they provide ways of using facts about the causal structure (notably, d-separation) to make inferences about conditional causal probabilities. I’ll now state all three rules. The intuition behind rules 2 and 3 won’t necessarily be entirely obvious, but after our discussion of rule 1 the remaining rules should at least appear plausible and comprehensible. I’ll have bit more to say about intuition below.

As above, we have a causal model on a graph

Rule 1: When can we ignore observations: Suppose

,z) = p(y|w,\mbox{do}(x)).")

Rule 2: When can we ignore the act of intervention: Suppose _{G_{\overline X,\underline Z}}")

,\mbox{do}(z)) = p(y|w,\mbox{do}(x),z).")

Rule 3: When can we ignore an intervention variable entirely: Let ")

_{G_{\overline X, \overline{Z(W)}}}")

,\mbox{do}(z)) = p(y|w,\mbox{do}(x)).")

In a sense, all three rules are statements of conditional independence. The first rule tells us when we can ignore an observation. The second rule tells us when we can ignore the act of intervention (although that doesn’t necessarily mean we can ignore the value of the variable being intervened with). And the third rule tells us when we can ignore an intervention entirely, both the act of intervention, and the value of the variable being intervened with.

I won’t prove rule 2 or rule 3 – this post is already quite long enough. (If I ever significantly revise the post I may include the proofs). The important thing to take away from these rules is that they give us conditions on the structure of causal models so that we know when we can ignore observations, acts of intervention, or even entire variables that have been intervened with. This is obviously a powerful set of tools to be working with in manipulating conditional causal probabilities!

Indeed, according to Pearl there’s even a sense in which this set of rules is complete, meaning that using these rules you can identify all causal effects in a causal model. I haven’t yet understood the proof of this result, or even exactly what it means, but thought I’d mention it. The proof is in papers by Shpitser and Pearl and Huang and Valtorta. If you’d like to see the proofs of the rules of the calculus, you can either have a go at proving them yourself, or you can read the proof.

Problems for the author

- Suppose the conditions of rules 1 and 2 hold. Can we deduce that the conditions of rule 3 also hold?

Using the causal calculus to analyse the smoking-lung cancer connection

We’ll now use the causal calculus to analyse the connection between smoking and lung cancer. Earlier, I introduced a simple causal model of this connection:

The great benefit of this model was that it included as special cases both the hypothesis that smoking causes cancer and the hypothesis that some hidden causal factor was responsible for both smoking and cancer.

It turns out, unfortunately, that the causal calculus doesn’t help us analyse this model. I’ll explain why that’s the case below. However, rather than worrying about this, at this stage it’s more instructive to work through an example showing how the causal calculus can be helpful in analysing a similar but slightly modified causal model. So although this modification looks a little mysterious at first, for now I hope you’ll be willing to accept it as given.

The way I’m going to modify the causal model is by introducing an extra variable, namely, whether someone has appreciable amounts of tar in their lungs or not:

(By tar, I don’t mean “tar” literally, but rather all the material deposits found as a result of smoking.)

This causal model is a plausible modification of the original causal model. It is at least plausible to suppose that smoking causes tar in the lungs and that those deposits in turn cause cancer. But if the hidden causal factor is genetic, as the tobacco companies argued was the case, then it seems highly unlikely that the genetic factor caused tar in the lungs, except by the indirect route of causing those people to smoke. (I’ll come back to what happens if you refuse to accept this line of reasoning. For now, just go with it.)

Our goal in this modified causal model is to compute probabilities like ) = p(y| \mbox{do}(x))")

, p(z|y)")

This means that we can determine )")

In other words, the causal calculus lets us do something that seems almost miraculous: we can figure out the probability that someone would get cancer given that they are in the smoking group in a randomized controlled experiment, without needing to do the randomized controlled experiment. And this is true even though there may be a hidden causal factor underlying both smoking and cancer.

Okay, so how do we compute

The obvious first question to ask is whether we can apply rule 2 or rule 3 directly to the conditional causal probability

If rule 2 applies, for example, it would say that intervention doesn’t matter, and so ) = p(y|x)")

If rule 3 applies, it would say that

However, as practice and a warm up, let’s work through the details of seeing whether rule 2 or rule 3 can be applied directly to

For rule 2 to apply we need _{G_{\underline X}}")

Obviously,

What about rule 3? For this to apply we’d need _{G_{\overline X}}")

Again,

Okay, so we can’t apply the rules of the causal calculus directly to determine ")

![[2] \,\,\,\, p(y| \mbox{do}(x)) = \sum_z p(y|z,\mbox{do}(x)) p(z|\mbox{do}(x)).](https://s0.wp.com/latex.php?latex=+%5B2%5D+%5C%2C%5C%2C%5C%2C%5C%2C+p%28y%7C+%5Cmbox%7Bdo%7D%28x%29%29+%3D+%5Csum_z+p%28y%7Cz%2C%5Cmbox%7Bdo%7D%28x%29%29+p%28z%7C%5Cmbox%7Bdo%7D%28x%29%29.+&bg=ffffff&fg=000000&s=0 "[2] \,\,\,\, p(y| \mbox{do}(x)) = \sum_z p(y|z,\mbox{do}(x)) p(z|\mbox{do}(x)).")

Of course, saying an experienced probabilist would instinctively do this isn’t quite the same as explaining why one should do this! However, it is at least a moderately obvious thing to do: the only extra information we potentially have in the problem is

Exercises

- I used without proof the equation

. This should be intuitively plausible, but really requires proof. Prove that the equation is correct.

To simplify the right-hand side of equation [2], we first note that we can apply rule 2 to the second term on the right-hand side, obtaining ) = p(z|x)")

_{G_{\underline X}}")

![[3] \,\,\,\, p(y| \mbox{do}(x)) = \sum_z p(y|z,\mbox{do}(x)) p(z|x).](https://s0.wp.com/latex.php?latex=+%5B3%5D+%5C%2C%5C%2C%5C%2C%5C%2C+p%28y%7C+%5Cmbox%7Bdo%7D%28x%29%29+%3D+%5Csum_z+p%28y%7Cz%2C%5Cmbox%7Bdo%7D%28x%29%29+p%28z%7Cx%29.+&bg=ffffff&fg=000000&s=0 "[3] \,\,\,\, p(y| \mbox{do}(x)) = \sum_z p(y|z,\mbox{do}(x)) p(z|x).")

At this point in the presentation, I’m going to speed the discussion up, telling you what rule of the calculus to apply at each step, but not going through the process of explicitly checking that the conditions of the rule hold. (If you’re doing a close read, you may wish to check the conditions, however.)

The next thing we do is to apply rule 2 to the first term on the right-hand side of equation [3], obtaining ) = p(y|\mbox{do}(z),\mbox{do}(x))")

")

) = p(y|\mbox{do}(z))")

![[4] \,\,\,\, p(y| \mbox{do}(x)) = \sum_z p(y|\mbox{do}(z)) p(z|x).](https://s0.wp.com/latex.php?latex=+%5B4%5D+%5C%2C%5C%2C%5C%2C%5C%2C+p%28y%7C+%5Cmbox%7Bdo%7D%28x%29%29+%3D+%5Csum_z+p%28y%7C%5Cmbox%7Bdo%7D%28z%29%29+p%28z%7Cx%29.+&bg=ffffff&fg=000000&s=0 "[4] \,\,\,\, p(y| \mbox{do}(x)) = \sum_z p(y|\mbox{do}(z)) p(z|x).")

So this means that we’ve reduced the computation of )")

")

) = \sum_x p(y|x,\mbox{do}(z)) p(x|\mbox{do}(z)).")

Now we’re cooking! Rule 2 lets us simplify the first term to ")

")

) = \sum_x p(y|x,z) p(x)")

![[5] \,\,\,\, p(y| \mbox{do}(x)) = \sum_{x'z} p(y|x',z) p(z|x) p(x') .](https://s0.wp.com/latex.php?latex=++%5B5%5D+%5C%2C%5C%2C%5C%2C%5C%2C+p%28y%7C+%5Cmbox%7Bdo%7D%28x%29%29+%3D+%5Csum_%7Bx%27z%7D+p%28y%7Cx%27%2Cz%29+p%28z%7Cx%29+p%28x%27%29+.+&bg=ffffff&fg=000000&s=0 "[5] \,\,\,\, p(y| \mbox{do}(x)) = \sum_{x'z} p(y|x',z) p(z|x) p(x') .")

This is the promised expression for ")

Something that bugs me about the derivation of equation [5] is that I don’t really know how to “see through” the calculations. Yes, it all works out in the end, and it’s easy enough to follow along. Yet that’s not the same as having a deep understanding. Too many basic questions remain unanswered: Why did we have to condition as we did in the calculation? Was there some other way we could have proceeded? What would have happeed if we’d conditioned on the value of the hidden variable? (This is not obviously the wrong thing to do: maybe the hidden variable would ultimately drop out of the calculation). Why is it possible to compute causal probabilities in this model, but not (as we shall see) in the model without tar? Ideally, a deeper understanding would make the answers to some or all of these questions much more obvious.

Problems for the author

- Why is it so much easier to compute

- Suppose we have a causal model

a subset of vertices for which all conditional probabilities are known. Is it possible to give a simple characterization of for which subsets

Unfortunately, I don’t know what the experimentally observed probabilities are in the smoking-tar-cancer case. If anyone does, I’d be interested to know. In lieu of actual data, I’ll use some toy model data suggested by Pearl; the data is quite unrealistic, but nonetheless interesting as an illustration of the use of equation [5]. The toy model data is as follows:

(1) 47.5 percent of the population are nonsmokers with no tar in their lungs, and 10 percent of these get cancer.

(2) 2.5 percent are smokers with no tar, and 90 percent get cancer.

(3) 2.5 percent are nonsmokers with tar, and 5 percent get cancer.

(4) 47.5 percent are smokers with tar, and 85 percent get cancer.

In this case, we get:

) = 45.25 \")

By contrast,  = 47.5")

= 85.25")

Summing up the general lesson of the smoking-cancer example, suppose we have two competing hypotheses for the causal origin of some effect in a system, A causes C or B causes C, say. Then we should try to construct a realistic causal model which includes both hypotheses, and then use the causal calculus to attempt to distinguish the relative influence of the two causal factors, on the basis of experimentally accessible data.

Incidentally, the kind of analysis of smoking we did above obviously wasn’t done back in the 1960s. I don’t actually know how causality was established over the protestations that correlation doesn’t impy causation. But it’s not difficult to think of ways you might have come up with truly convincing evidence that smoking was a causal factor. One way would have been to look at the incidence of lung cancer in populations where smoking had only recently been introduced. Suppose, for example, that cigarettes had just been introduced into the (fictional) country of Nicotinia, and that this had been quickly followed by a rapid increase in rates of lung cancer. If this pattern was seen across many new markets then it would be very difficult to argue that lung cancer was being caused solely by some pre-existing factor in the population.

Exercises

- Construct toy model data where smoking increases a person’s chance of getting lung cancer.

Let’s leave this model of smoking and lung cancer, and come back to our original model of smoking and lung cancer:

What would have happened if we’d tried to use the causal calculus to analyse this model? I won’t go through all the details, but you can easily check that whatever rule you try to apply you quickly run into a dead end. And so the causal calculus doesn’t seem to be any help in analysing this problem.

This example illustrates some of the limitations of the causal calculus. In order to compute )")

While this model is plausible, it is not beyond reproach. You could, for example, criticise it by saying that it is not the presence of tar deposits in the lungs that causes cancer, but maybe some other factor, perhaps something that is currently unknown. This might lead us to consider a causal model with a revised structure:

So we could try instead to use the causal calculus to analyse this new model. I haven’t gone through this exercise, but I strongly suspect that doing so we wouldn’t be able to use the rules of the causal calculus to compute the relevant probabilities. The intuition behind this suspicion is that we can imagine a world in which the tar may be a spurious side-effect of smoking that is in fact entirely unrelated to lung cancer. What causes lung cancer is really an entirely different mechanism, but we couldn’t distinguish the two from the statistics alone.

The point of this isn’t to say that the causal calculus is useless. It’s remarkable that we can plausibly get information about the outcome of a randomized controlled experiment without actually doing anything like that experiment. But there are limitations. To get that information we needed to make some presumptions about the causal structure in the system. Those presumptions are plausible, but not logically inevitable. If someone questions the presumptions then it may be necessary to revise the model, perhaps adopting a more sophisticated causal model. One can then use the causal calculus to attempt to analyse that more sophisticated model, but we are not guaranteed success. It would be interesting to understand systematically when this will be possible and when it will not be. The following problems start to get at some of the issues involved.

Problems for the author

- Is it possible to make a more precise statement than “the causal calculus doesn’t seem to be any help” for the original smoking-cancer model?

- Given a probability distribution over some random variables, it would be useful to have a classification theorem describing all the causal models in which those random variables could appear.

- Extending the last problem, it’d be good to have an algorithm to answer questions like: in the space of all possible causal models consistent with a given set of observed probabilities, what can we say about the possible causal probabilities? It would also be useful to be able to input to the algorithm some constraints on the causal models, representing knowledge we’re already sure of.

- In real-world experiments there are many practical issues that must be addressed to design a realiable randomized, controlled experiment. These issues include selection bias, blinding, and many others. There is an entire field of experimental design devoted to addressing such issues. By comparison, my description of causal inference ignores many of these practical issues. Can we integrate the best thinking on experimental design with ideas such as causal conditional probabilities and the causal calculus?

- From a pedagogical point of view, I wonder if it might have been better to work fully through the smoking-cancer example before getting to the abstract statement of the rules of the causal calculus. Those rules can all be explained and motivated quite nicely in the context of the smoking-cancer example, and that may help in understanding.

Conclusion

I’ve described just a tiny fraction of the work on causality that is now going on. My impression as an admittedly non-expert outsider to the field is that this is an exceptionally fertile field which is developing rapidly and giving rise to many fascinating applications. Over the next few decades I expect the theory of causality will mature, and be integrated into the foundations of disciplines ranging from economics to medicine to social policy.

Causal discovery: One question I’d like to understand better is how to discover causal structures inside existing data sets. After all, human beings do a pretty good (though far from perfect) job at figuring out causal models from their observation of the world. I’d like to better understand how to use computers to automatically discover such causal models. I understand that there is already quite a literature on the automated discovery of causal models, but I haven’t yet looked in much depth at that literature. I may come back to it in a future post.

I’m particularly fascinated by the idea of extracting causal models from very large unstructured data sets. The KnowItAll group at the University of Washington (see Oren Etzioni on Google Plus) have done fascinating work on a related but (probably) easier problem, the problem of open information extraction. This means taking an unstructured information source (like the web), and using it to extract facts about the real world. For instance, using the web one would like computers to be able to learn facts like “Barack Obama is President of the United States”, without needing a human to feed it that information. One of the things that makes this task challenging is all the misleading and difficult-to-understand information out on the web. For instance, there are also webpages saying “George Bush is President of the United States”, which was probably true at the time the pages were written, but which is now misleading. We can find webpages which state things like “[Let’s imagine] Steve Jobs is President of the United States“; it’s a difficult task for an unsupervised algorithm to figure out how to interpret that “Let’s imagine”. What the KnowItAll team have done is made progress on figuring out how to learn facts in such a rich but uncontrolled environment.

What I’m wondering is whether such techniques can be adapted to extract causal models from data? It’d be fascinating if so, because of course humans don’t just reason with facts, they also reason with (informal) causal models that relate those facts. Perhaps causal models or a similar concept may be a good way of representing some crucial part of our knowledge of the world.

Problems for the author

- What systematic causal fallacies do human beings suffer from? We certainly often make mistakes in the causal models we extract from our observations of the world – one example is that we often do assume that correlation implies causation, even when that’s not true – and it’d be nice to understand what systematic biases we have.

- Humans aren’t just good with facts and causal models. We’re also really good at juggling multiple causal models, testing them against one another, finding problems and inconsistencies, and making adjustments and integrating the results of those models, even when the results conflict. In essence, we have a (working, imperfect) theory of how to deal with causal models. Can we teach machines to do this kind of integration of causal models?

- We know that in our world the sun rising causes the rooster to crow, but it’s possible to imagine a world in which it is the rooster crowing that causes the sun to rise. This could be achieved in a suitably designed virtual world, for example. The reason we believe the first model is correct in our world is not intrinsic to the data we have on roosters and sunrise, but rather depends on a much more complex network of background knowledge. For instance, given what we know about roosters and the sun we can easily come up with plausible causal mechanisms (solar photons impinging on the rooster’s eye, say) by which the sun could cause the rooster to crow. There do not seem to be any similarly plausible causal models in the other direction. How do we determine what makes a particular causal model plausible or not? How do we determine the class of plausible causal models for a given phenomenon? Can we make this kind of judgement automatically? (This is all closely related to the last problem).

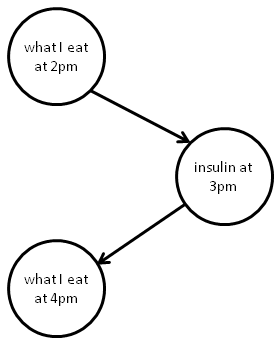

Continuous-time causality: A peculiarity in my post is that even though we’re talking about causality, and time is presumably important, I’ve avoided any explicit mention of time. Of course, it’s implicitly there: if I’d been a little more precise in specifying my models they’d no doubt be conditioned on events like “smoked at least a pack a day for 10 or more years”. Of course, this way of putting time into the picture is rather coarse-grained. In a lot of practical situations we’re interested in understanding causality in a much more temporally fine-grained way. To explain what I mean, consider a simple model of the relationship between what we eat and our insulin levels:

This model represents the fact that what we eat determines our insulin levels, and our insulin levels in turn play a part in determining how hungry we feel, and thus what we eat. But as a model, it’s quite inadequate. In fact, there’s a much more complex feedback relationship going on, a constant back-and-forth between what we eat at any given time, and our insulin levels. Ideally, this wouldn’t be represented by a few discrete events, but rather by a causal model that reflects the continual feedback between these possibilities. What I’d like to see developed is a theory of continuous-time causal models, which can address this sort of issue. It would also be useful to extend the calculus to continuous spaces of events. So far as I know, at present the causal calculus doesn’t work with these kinds of ideas.

Problems for the author

- Can we formulate theories like electromagnetism, general relativity and quantum mechanics within the framework of the causal calculus (or some generalization)? Do we learn anything by doing so?

Other notions of causality: A point I’ve glossed over in the post is how the notion of causal influence we’ve been studying relates to other notions of causality.

The notion we’ve been exploring is based on the notion of causality that is established by a (hopefully well-designed!) randomized controlled experiment. To understand what that means, think of what it would mean if we used such an experiment to establish that smoking does, indeed, cause cancer. All this means is that in the population being studied, forcing someone to smoke will increase their chance of getting cancer.

Now, for the practical matter of setting public health policy, that’s obviously a pretty important notion of causality. But nothing says that we won’t tomorrow discover some population of people where no such causal influence is found. Or perhaps we’ll find a population where smoking actively helps prevent cancer. Both these are entirely possible.

What’s going on is that while our notion of causality is useful for some purposes, it doesn’t necessarily say anything about the details of an underlying causal mechanism, and it doesn’t tell us how the results will apply to other populations. In other words, while it’s a useful and important notion of causality, it’s not the only way of thinking about causality. Something I’d like to do is to understand better what other notions of causality are useful, and how the intervention-based approach we’ve been exploring relates to those other approaches.

Acknowledgments

Thanks to Jen Dodd, Rob Dodd, and Rob Spekkens for many discussions about causality. Especial thanks to Rob Spekkens for pointing me toward the epilogue of Pearl’s book, which is what got me hooked on causality!

Principal sources and further reading

A readable and stimulating overview of causal inference is the epilogue to Judea Pearl’s book. The epilogue, in turn, is based on a survey lecture by Pearl on causal inference. I highly recommend getting a hold of the book and reading the epilogue; if you cannot do that, I suggest looking over the survey lecture. A draft copy of the first edition of the entire book is available on Pearl’s website. Unfortunately, the draft does not include the full text of the epilogue, only the survey lecture. The lecture is still good, though, so you should look at it if you don’t have access to the full text of the epilogue. I’ve also been told good things about the book on causality by Spirtes, Glymour and Scheines, but haven’t yet had a chance to have a close look at it. An unfortunate aspect of the current post is that it gives the impression that the theory of causal inference is entirely Judea Pearl’s creation. Of course that’s far from the case, a fact which is quite evident from both Pearl’s book, and the Spirtes-Glymour-Scheines book. However, the particular facets I’ve chosen to focus on are due principally to Pearl and his collaborators: most of the current post is based on chapter 3 and chapter 1 of Pearl’s book, as well as a 1994 paper by Pearl, which established many of the key ideas of the causal calculus. Finally, for an enjoyable and informative discussion of some of the challenges involved in understanding causal inference I recommend Jonah Lehrer’s recent article in Wired.

Interested in more? Please follow me on Twitter. You may also enjoy reading my new book about open science, Reinventing Discovery.

Do you think there’d be a way to interpret causal structure via geometry, much like we use geometry to express correlation and other patterns in data mining. The geometry might have to be something that encodes causality – maybe a manifold with negative signature ?

@Suresh – Fascinating idea! No idea if it’s possible, though, the thought never crossed my mind. I guess I think of causal models as having an inherent directionality, due to the dag structure, while most geometries don’t have the same kind of directionality. But maybe there’s some trick to get around that.

There’s been plenty of work on the geometry of curved exponential families, and their relation to inference in graphical models. See, as a start, e.g.

http://uai.sis.pitt.edu/papers/98/p472-settimi.pdf

http://projecteuclid.org/euclid.aos/1009210550

http://arxiv.org/abs/math/0301255

Bernd Sturmfels and Lior Pachter also have a pretty good book that touches on a lot of this —

http://bio.math.berkeley.edu/ascb/

Yes, I’m aware of that work. But the geometry there is a geometry in the parameter space. I don’t think it can be used to capture this kind of causality (at least at first glance)

Here’s a nice example of how A implies B is often popularly assumed to mean “B hence caused by A” http://www.nhs.uk/conditions/oral-thrush—adults/Pages/Introduction.aspx

I came across this as I was interested in oral thrush. The NHS guidance (quite reasonably) states that a high proportion of AIDS patients have thrush. Thrush has many causes and is correlated with use of inhaled steroids. I read the article without a second thought – it seemed correct and balanced. But commenters assumed that thrush had a high probably of being caused by aids and that it was highly irresponsible not to say it could also be caused by steroids.

This is a typical example of Bayes – the a priori chance of having AIDS is lower (I think) than being on Oral steroids

I don’t know the answer. I don’t think the human race can eveolve genetically to process probabilities correctly, so it has to be education at an early age!

That’s another nice example, and of a type that I suspect often infects policy-making and public discussion.

1. If there’s an alternative ??? path from smoking to lung cancer it may be possible to put bounds on P(cancer|dio(smoking)) even if you can’t compute it exactly.

2. Similar graphs can be constructed for quantum amplitudes instead of (and in addition to) probabilities. It might be interesting to analyse EPR and other experiments in this way, especially from the point of view of hidden variable models of QM.

Thanks for this very informative post. Let me just make a few comments about your “physics” question:

“Can we formulate theories like electromagnetism, general relativity and quantum mechanics within the framework of the causal calculus (or some generalization)? Do we learn anything by doing so?”

I have been working on formulating quantum theory in a Bayesian network language, which is an obvious precursor to developing a causal calculus for it. Even that problem is not so simple, given that the standard formalism has an assumed causal structure built into it, which we need to get rid of before we start. My recent papers with Rob Spekkens are part of an attempt to do that.

One lesson that I have learned from this is that we need to get away from the usual “initial state+dynamics” way of looking at physics in order to fit it into this framework. Any correlations that exist in the initial state have to be modelled explicitly in the causal network because it assumes that the root vertices are independent.

Finally, let me just mention that you might be able to get away with a simpler structure for modelling causality in deterministic theories like electromagnetism. Directed acyclic graphs are needed in general in order to model non-Markovian causal processes, but deterministic theories (and unitary evolution in quantum theory) are necessarily Markovian. Therefore, you should be able to get away with just using a poset to model causality in these cases, the corresponding DAG being just the Hasse diagram of the poset. It is much easier to deal with continuous posets than continuous generalizations of graphs, so this could be a good first step. By the way, this explains why Raphael Sorkin et. al. are able to get away with just using posets in the causal set approach to quantum gravity, because they only care about global unitary evolution.

Thanks for the pointer to your work, Matt, it sounds fascinating. Although I’ve chatted with Rob about this, I didn’t realize that you were trying to formulate quantum theory in terms of Bayesian networks. (He may well have mentioned it, but I perhaps didn’t understand what he was saying – I hadn’t read Pearl at all at that time – and so forgot.)

Nice exposition! Perhaps some notion of “latent surprise” could be relevant. Adapting from the Wired article you cite, imagine that a candidate drug’s operation has two plausible causal models. The first and most plausible model is simple. It is used during drug development. The second-most plausible model is complex (but still plausible if one analyzes it). If that second-most plausible causal model is very different from the first, that could be a “latent surprise” for researchers – a warning that, if their understanding of the drug’s operation changes somewhat, the clinical effects could be profound.

In general, if the most plausible few models are close (in the metric of plausibility) yet very different (in the metric space of causal model similarity), this is a warning of big latent surprises if our understanding shifts a bit. Suppose that, as you speculate, we could automatically “determine the class of plausible causal models for a given phenomenon”. We might then also be able to scan automatically for latent surprises in important systems: scientific, social, financial, policy, and so forth.

You mentioned the following: “Obviously, it’d make no sense to have loops in the graph: We can’t have causing causing causing ! At least, not without a time machine.”

Loops in causality DAG can be created without time machines as follows.

1. In some distant origin that is not in the history of measurements, A caused B;

2. B caused C;

3. C caused A;

4. so on and so forth.

5. Over time, A, B, and C have caused other variables due to unknown reasons.

So, to the observer, A caused B, which caused C, which (in turn) caused A. This situation could happen in Human History due to lapses in measurement and in Astronomy because the lifetime of the observed (universe) is much longer than the lifetime of the observer (humans).

Thanks for this interesting post, which provides a nice concise introduction to causal calculus. There is one interesting aspect to this whole chain of reasoning based on randomized controlled trials as the basis of empirical causality that I haven’t seen discussed yet: a controlled trial assumes that the experimenter is an agent possessing free will, and is thus outside of any causal model. There is a recent tendency in the scientific community (see this article for example, and my comments on it) to claim that free will does not exist, and that human behavior is governed entirely by molecular processes (and thus ultimately quantum physics). With that assumption, whatever an experimenter does is merely one more observable in a stochastic network, randomized controlled trials disappear, and causal calculus disappears as well. We arrive at the conclusion that the only scientific method to attribute causality relies on the existence of free will as a source of “obvious” causality.

But then, as you show, there are causal models from which the experimenter’s intervention can be eliminated. We can thus draw conclusions about causality without assuming the “obvious” source of free will. I wonder if it is possible to state under which conditions a causal model permits this elimination. Rules 2 and 3 are about individual variables, but is there a rule that applies to a complete graph?

Thanks for this. I’ve been spending a lot of time thinking about Pearl’s book lately and this is by far the most accessible introduction to the material that I have come across.

One quick correction. Close to the end of your discussion of rule 1 (2 paragraphs before the heading: “the rules of the causal calculus”), you give the equation:

P(y|do(x),z) = P(y|do(x),z)

Presumably you mean:

P(y|do(x),z) = P(y|do(x))

Thanks, I’ve corrected it!

Of interest for our question about algorithms: http://www.phil.cmu.edu/projects/tetrad/.

“Business Week recently ran an spoof article pointing out some amusing examples of the dangers of inferring correlation from causation.”

Probably you meant the other way around: “amusing examples of the dangers of inferring causation from correlation”?

Thanks, fixed!

I have enjoyed a lot reading this. I am slightly confused about the wording of the following sentence:

where f_j is a function, and Y_j is a collection of random variables such that: (a) the Y_j,. are independent of one another for different values of j; and (b) for each j, Y_j,. is independent of all variables X_k, except when X_k is X_j itself, or a descendant of X_j. The intuition is that the are a collection of auxiliary random variables which inject some extra randomness into X_j (and, through X_j, its descendants), but which are otherwise independent of the variables in the causal model.

What you mean by that is that for instance in the diagram above the paragraph Y_4,i is not independent of X_3 and X_2?

No the Y_4,i’s are independent of X_3 and X_2.

The only way this could fail is if condition (b) is met. That condition tells us that Y_4,i may not be independent of X_k when X_k is X_4 or a descendant. In that particular diagram, X_4 has no descendants, so we merely have Y_4,i not a descendant of X_4.

Thanks for writing this up. It was very helpful!

Regarding eq [5], you commented that it wasn’t transparent. If I’m not mistake, you can reduce this to

\sum_z P(z|x)P(y,z),

which is much more transparent.

How do you do this?

My mistake. I thought I had marginalized out the x’, but didn’t.

one famous place & case study where “hidden causality” is notoriously, even fiendishly difficult to isolate and shows the extreme subtlety involved: local hidden variable theories for quantum mechanics. which recently have been brought back from the dead (or maybe semi zombie state) by anderson/brady in a soliton model. more thoughts on that here. it has an aura of unorthodoxy but lets not forget that the greats have always been enamored with the idea. einstein, schroedinger, ‘t hooft, etcetera.

part of the difficulty in QM is the idea of counterintuitive variables that might actually cause the experiment apparatus to “measure” or “not measure” (or “click” vs “not click/silent”). this has been called a “conspiracy” for decades. not sure who invented that description.

http://www.sciencemag.org/content/338/6106/496.full.html

Goes into causal detection based upon ‘prediction when variable A has been removed’, and why correlation sometimes makes causal detection worse, not better.

Imply causation? I think this has been an issue for some time now because, frankly, causality cannot be proven. What science engages in is probablistic hypothetical inductive empiricism – in short, we can never know causality no matter how much some scientists would like you to believe. Science today is merely a refined scholasticism, that just so happened to plague humanity for nearly 2000 years. Not a single person can or has or will prove (analytically) universal causality of Being – to put it in easier terms, someone prove to me gravity will exist next Tuesday…

Realy interesting!

Interesting article overall, but I disagree with this statement:

We can’t have X causing Y causing Z causing Y!

In fact, this is called positive feedback loop and is common in nature. You will find a lot of examples in wikipedia, none of them needs a time machine 😉

I noticed I incorrectly quoted you above, but the point is, loops in causal diagrams are common.

The labels in the diagrams aren’t just for broad classes of phenomena, they’re labels for random variables. A reasonable informal way of thinking is that this means you should think of the nodes as referring to specific events.

Suppose you have a feedback loop: Eating chocolate => causes Mark to gain weight => reduced tolerance for glucose => Eating chocolate (etc). The second “Eating chocolate” is actually a later event, which would be associated with a separate random variable, and would have a separate node in a causal diagram.

Incidentally, that informal way of thinking – nodes as specific events in time – isn’t the full story. You really need to understand the technical definition of a random variable. But this informal approach conveys the gist of what’s going on.

In [1], I’m confused how to expand the right side; I don’t see where I can get the values for pa(Xj).

I’m trying to expand the basic cancer-smoking-hidden model in terms of basic probabilities, and I can only get as far as P(gets cancer | do(smokes)) = P(gets cancer, smokes) / P(smokes | pa(Smoke)).

(My end goal is to see if I can use [1] to expand the cancer-smoking-tar-hidden model and obtain the same result that you did, but without using the causal calculus.)

pa(.) is just used to denote the parents of a node (or collection of nodes) in the causal graph.

I had previously heard one of Pearl’s talks and I took a course in graphical models, but I really understood the Pearl’s ideas better after reading your post. Thanks.

Cheers, Hein

Hello, thanks for this nice explanation of Pearl’s & al. theory.

But there is something I can’t grasp in spite of reading Pearl’s lecture slides or some parts of his papers.

When simplifying equation [2], you say (as Pearl does) that we can apply rule 2 to find : p(z|do(x)) = p(z|x)

But rule 2 is much more complex than this. It tells about x,y,z and w.

How can you make disappear y and w in rule 2 ? Is it because w is unobserved ? Is it because pa(y) = x and we can use another relation ?

Thanks for your help

Okay, after many readings , I guess I’m now able to answer to myself.

In the 1992 paper, Pearl derives three properties from [1] formula.

The third is :

p(z|do(x)) = p(z|x) iff z_|_ pa(x) | x

which is the case in the example graph.

Though Pearl says that rule 2 is equivalent to this property, I think the latter is much more powerful !

I am trying to understand your eq. [5]; when I set up the calculations in a spreadsheet table, I get the following result, namely no difference between P(cancer) and P(cancer|do(smoking)), which is what I intuitively expected. Can you tell me where I went wrong?

z x’ P(y|x’,z) p(x’) p(z,x’) p(z|x’)

no tar no smoke 0.1 0.5 0.475 0.95 0.0475

no tar smoke 0.9 0.5 0.025 0.05 0.0225

tar no smoke 0.05 0.5 0.025 0.05 0.00125

tar smoke 0.85 0.5 0.475 0.95 0.40375

total 0.475

Regarding the application of Simpson’s Paradox to the Civil Rights Act and your mention of application to gender bias I would ask, how far can one go in “slicing and dicing”? How often is this an exercise in merely seeking an outcome that supports one’s pre-existing bias? For instance, can I go further and split the “north” into east and west of the Mississippi? Suppose this how the the votes came out with this further split (recall we had DemNorth(145/154), RepNorth(138/162)):

North-East: Dem(129/134 .966)

North-West: Dem(16/20 = .8) Rep(109/132 >.825)

Now we have three regions, NorthEast, NorthWest, and South and the republican % was higher in two out of three. Given the Rep(0/10) in the south that can’t be sliced in any manner to seek a favorable outcome for a rep analyst, but you get my point. I just quickly jotted down a few trials to come up with this example which is not surprising given the initial split into north-south is just a first iteration that demonstrates this is possible. But again I ask, where does the slicing and dicing stop in such an analysis? Usually with these sorts of political and judicial analyses, those things that involve human motivations, it usually stops where the desired outcome is achieved – and the best part is – one can claim it was scientific and mathematical so is indisputable! The analyst can say under oath and with a straight face,”I lay the numbers before you and the numbers don’t lie.” But just what do the numbers tell us?

Your threshold “being Republican, rather than Democrat, was an important factor in causing someone to vote for the Civil Rights Act” is also subjective – as it must be in dealing with human motivations, e.g. what is ‘important’?, what is ‘causing’? One could note the 94Dem/10Rep representation from the south, and analyzing the majority of southern voter’s motivations at that time conclude that a major reason for the big Dem majority in that region was in part caused by the voter’s view that based on platforms and reputation, being Rep, the losing challenger was most likely in favor of the Civil Rights Act.

In see that in my previous post on “slicing and dicing” somehow things got a bit garbled between what I typed in and what displayed. One could derive the details given what did display but here is what I intended regarding the East-West split of the North in the Civil Rights vote split:

North-East: Dem(129/134).966

North-West Dem(16/20)=.80 Rep(109/132)>,825

I’ve applied Simpson’s Paradox to the North vote split. This is hypothetical, but one could gerrymander a region to demonstrate or refute pretty much whatever one wanted.

Great post!

Sorry I’m a little late to the party… but I’ve been busy doing a lot of work in what I’m calling a “science of conceptual systems” where a conceptual system is a set of interrelated concepts (theories, models, mental models, policies, strategic plans, etc.).

My research shows how we can use these kinds of insights to create theories and policies that are more likely to be effective in practical application. You can access some of my writings at: http://projectfast.org/category/research/articles/

be sure to check out this one in particular: http://projectfast.org/the-structure-of-theory-and-the-structure-of-scientific-revolutions-what-constitutes-an-advance-in-theory/

There, i analyze the evolution of a theory of physics from ancient times through the scientific revolution. By focusing on causal relationships, and concatenated relationships between nodes, we gain rather useful insights into how to create more effective theories and policies.

This is important because, within the social sciences, our current theories fail far more often than they succeed. imagine what we might be able to accomplish if our economic policies worked twice as well as they do? What about theories of management and psychology? Double the effectiveness and watch what happens to organizational and mental health!

Thanks,

Steve

> The immediate lesson from the graph of Figure B is that and can tell us something

> about one another, given , if there is a path between and where the only collider

> is at . In fact, the same phenomenon can occur even in this graph:

In the example you gave about the music academy, and Berkson’s paradox, there should be another node in the graph: that X gives information about Y if and only if X and Y have some other (external) connection. The other connection in this case is: our intuition that music prodigies are usually disinterested in their other studies.

So, you cannot proceed to the principle that when X –> Z <– Y, X gives information about Y, i.e. that the path is unblocked. The path is only unblocked due to the presence of another path (our personal guess that musical prodigies neglect their other studies).

> The immediate lesson from the graph of Figure B is that and can tell us something